Fundamentals of industry analysis refer to the systematic evaluation of an industry’s structure, dynamics, growth potential, and competitive environment to assess the prospects of companies operating within that industry. It involves examining factors such as industry definition, market size, cyclicality, demand drivers, secular trends, competitive intensity, regulatory environment, and the industry life cycle. Through industry analysis, analysts can understand how economic conditions, technological changes, and market forces influence the performance and profitability of businesses within the industry. This analysis helps investors and researchers identify growth opportunities, competitive advantages, and potential risks, thereby supporting more informed investment and strategic decisions.

Table of Contents

- Role of Industry Analysis in Fundamental Analysis

- Defining the Industry

- Understanding Industry Cyclicality

- Market Sizing and Trend Analysis

- Secular Trends, Value Migration and Business Life Cycle

- Understanding the Industry Landscape

Check out NISM X Taxmann's Research Analyst which is a comprehensive, practice-oriented handbook on equity research and investment analysis, designed as a complete desk reference for conducting professional research in regulated capital markets. It seamlessly integrates securities market fundamentals, research methodologies, economic and industry analysis, company evaluation, valuation, risk assessment, and research report writing into a single, coherent framework. The book traces the entire equity research lifecycle—from market understanding to valuation and compliant research output—while emphasising disciplined analytical thinking, sound professional judgment, and ethical conduct. Published by Taxmann, it is an essential resource for research professionals, analysts, students, and educators seeking a rigorous and practical approach to high-quality equity research.

1. Role of Industry Analysis in Fundamental Analysis

Economic analysis helps us understand whether economy, in general, is likely to grow in the foreseeable future or decline. Industry analysis helps in understanding how each industry would be impacted under the current economic conditions.

In Industry analysis, analysts also try to understand how the various players related to a particular industry or business sector are likely to react and how that may affect the prospect of the industry. The words Industry and Business Sector or Economic Sector are sometimes a source of confusion due to their lose usage and the multitude of definitional standards across the globe. Industry is a grouping of firms, which offer the same or similar products or service to serve the same customer need (example, Auto industry, Insurance industry, Steel industry, Telecom industry, Entertainment industry). Business Sector is a broad category comprising similar and related industries (example, Financial Services Sector encompassing Insurance, Banking, Credit Rating, Investment Banking; Industrial metals sector comprising Steel, Copper, and Aluminum industries). Economic sector represents the segments of an economy which contribute to the total national income or national product, like agriculture, manufacturing, public utilities, and services. For the research analysts the following paragraphs would bring in more clarity.

The various questions that must be addressed in industry analysis include the following:

- What is the industry in which the company operates?

- How much does it get impacted on account of cyclical trends in the economy?

- What is the potential industry size?

- How has the industry been performing in the past and what were the drivers behind the performance?

- What is the level of competition in the industry? How does it affect the pricing power of the various players?

- What are the various secular trends that affect the industry, and are they causing any value migration?

- Are there any regulatory headwinds or tail winds affecting the industry?

2. Defining the Industry

The very first step in an industry analysis is to define the industry in which the company operates. Industry definition is not always an easy task. While there are several standard industry classification systems, such as National Industry Classification (NIC) system in India, the Global Industry Classification Standard (GICS). or North American Industry Classification System (NAICS) in US, they may not necessarily capture the substance of the industry.

For instance, NIC has a single classification for manufacture of passenger cars. Thus, every car manufacturer including entry level compact car manufacturers and high-end luxury car manufacturers fall under the same industry classification. However, since the dynamics of the luxury car manufacturer is very different from entry level passenger car segment, analysts may view them as different industries. The challenge especially increases when a company competes in many industries to earn its income.

Let us take the example of PVR Limited. On one hand, PVR Cinemas competes with satellite channels and Over the Top (OTT) platforms, such as Netflix and Hotstar, to attract audience. On the other hand, the cinema industry also competes with live theatres, live performances, and sporting leagues.

Thus, if an analyst applies a narrow industry definition and classifies the company as part of cinema exhibitors, it creates a risk of overlooking other competitors. But if one were to give broader definition, then challenge is to identify whether to classify the company as part of entertainment media industry or should it be classified as part of Out of Home (OOH) entertainment industry. This may force the analyst to classify it as part of a much broader media and entertainment industry. But that would create another challenge as each segment within this broader group have their own idiosyncrasies and not strictly comparable. This understanding is extremely crucial, especially when the analysts embark on the journey of comparison of financials, finds our peer firms, and then undertakes valuations.

Camera manufacturing is another example that shows the challenges in defining an industry. Couple of decades ago, cameras were a standalone product. However, with the emergence of mobile phones with built-in cameras, a lot of entry level digital cameras started losing their sales to these phones. Today, with emergence of high technology mobile phones, even mid-tier cameras are facing competition from mobile phones. If cameras are defined as a standalone industry, then an analyst may end up ignoring this huge competition from mobile phones.

An analyst should carefully consider the various factors that drive the business and should classify it as part of the industry group which have such common driving factors. Thus, if an analyst believes that PVR Limited’s business is driven by people’s propensity to spend time outside their home, it may be appropriate to classify it as part of out of home entertainment industry. On the other hand, if the business is largely driven by people’s propensity to consume movie content, then it may be appropriate to classify it as part of entertainment media.

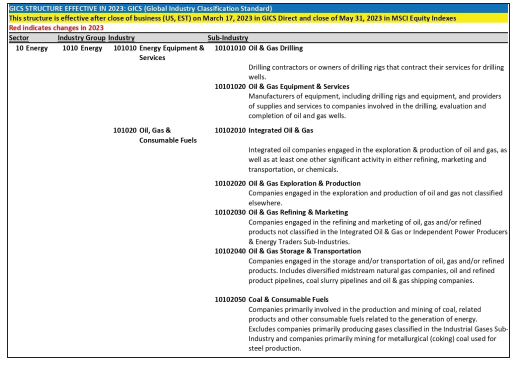

GICS which is widely used in financial sector for global investors on the other hand is a four-tiered, hierarchical industry classification system where the four tiers are – Sectors, Industry Groups, Industries and Sub-Industries divided into 11 sectors, 25 industry groups,74 industries and 163 sub-industries. An example for grouping for Energy sector is shown below for illustration purposes:

Source – MSCI, March 2023

3. Understanding Industry Cyclicality

Economic cycles affect all businesses. However, they affect some businesses more than others. Based on the cyclical nature, industries can be classified into three categories:

Defensive Industries – These are industries that create products and services that have low-income elasticity i.e., a fall or rise in income does not affect the demand significantly. Therefore, these industries experience minimal impact on account of economic cycles. Rather, their business prospects are affected only by secular trends. Food, agricultural inputs, and healthcare are some of the industries that have exhibited these traits in the past.

Semi-cyclical Industries – These industries experience growth in sales during the expansionary phase and decline during recessionary phase. However, these industries do have some base level demand which help the industry to have reasonably healthy sales in recessionary conditions also. Consumer durables industry has exhibited these traits.

Deep Cyclical Industries – These industries witness extreme cyclicality in their revenues as they are largely driven by economic cycle and/or commodity cycles. Capital goods industry or Steel exhibits such behavior. During recessionary conditions, their sales drop significantly as most companies put their capacity expansion plans on hold. However, these industries experience massive growth at the first signs of economic recovery as pent-up demand result in higher orders.

4. Market Sizing and Trend Analysis

Industries that are underpenetrated have high growth potential as there is more headroom for growth. However, as industries mature, the new growth avenues decline and the overall growth rates, thus, come down. Therefore, while studying industry, it is important to analyse the potential size of the market and current size of the market.

However, measuring the current market size is difficult especially if there are many unorganised players or private companies whose information is not available in public domain. Further, quantifying the potential size of the market also involves making lot of assumptions, which can go wrong.

Therefore, studying the past trends can supplement our analysis and help us understand how the industry has been growing and what are the factors that are affecting growth. Such studies also help us understand the underlying secular trends.

Market sizing can be done through either top-down approach or bottom-up approach. In a top-down approach, we measure the size of the market or industry starting from macro-economic factors and arrive up to the industry level. In bottom-up approach, we quantify the market by looking at individual companies and aggregating their data to arrive at the industry size.

For example, if we were to quantify the total industry size for a particular therapy, we can use the top-down approach as follows:

(i) identify how many patients underwent the therapy

(ii) ascertain average expenditure per patient

(iii) take the product of (i) and (ii) to arrive at the revenue.

From a bottom-up perspective, we can look at revenue of all the hospitals that provide this therapy and identify how much (or what proportion) of their revenue was earned from this therapy. We can then aggregate it to arrive at industry size.

As mentioned above, market sizing may involve making certain assumptions, as all the required information may not be available.

5. Secular Trends, Value Migration and Business Life Cycle

As discussed earlier, secular trends are long term trends that cause displacement in production or consumption of goods and services. There are various factors that drive secular trends:

(i) Technological Advancement – New technology can cause disruption in many ways. It can bring in new methodology in production of goods. It can provide alternative to an existing product or can create new consumption pattern. The following are some of the examples of secular trends caused by technology:

(a) Horizontal drilling technology enabled exploration of shale gas. This resulted in significant decline in long term average price of hydrocarbons.

(b) Digital cameras made film rolls obsolete; mobile cameras made entry level digital cameras obsolete.

(c) Improvement in battery technology is enabling increased use of electric vehicles compared to fossil fuel driven vehicles.

(ii) Change in Income Levels – As an economy grows, the disposable income of population is likely to increase. This can cause change in category of goods and services being consumed. People start consuming premium products compared to cheaper alternatives.

(iii) Demographic Changes – The composition of a country’s population in terms of age, gender and ethnicity may undergo change over a period. This may cause changes in the consumption pattern within the country. For example, ageing population in Japan has resulted in decrease in per capita consumption of beer.

(iv) Change in Culture, and Tastes and Preferences – Cultural changes are a constant. Most often, they are gradual. However, sometimes changes can also be sudden driven by revolution, insurgencies, or a societal response to a pandemic. These changes can cause a change in consumption pattern of goods and services. For example, increasing influence of western culture in Asian societies created higher demand for western clothing.

(v) Changes in Regulation or Government Policy – Change in regulations, or government actions may also create secular trends in industry. For instance, implementation of GST created certain efficiencies in the logistic industry. It in turn reduced the demand for purchase of new commercial vehicles.

In addition to the above, many other factors may also serve as a catalyst for a secular trend.

When a new secular trend emerges, it causes value migration between industries or between players. And often it also creates an inflection point in the business cycle of one or more affected industries.

5.1 Value Migration

In simple terms, value migration happens when a phenomenon creates long term advantage for one or more entities at the cost of other entities. Thus, the entity that gains witnesses an increase in its shareholder value, while the other entity loses. The entity that adopts the latest technology, or captures the changing needs of the customer preferences, or creates a disrupting innovation benefit and its laggard competitors loose.

Such a shift can happen across geographies, across industries, across the value chain and to a lesser extent between competitors within the industry.

Geographic Migration – Geographic migration of value happens when a secular trend helps a country or geography as compared to other. For instance, horizontal drilling and shale gas discovery shifted value to US based oil exploration at the cost of other oil producing countries as US had large amount of shale gas reserve and were able to extract them at a lower cost compared to other oil producing nation. Similarly, globalization helped low-cost manufacturer such as China to rapidly grow its economy as compared to many other high cost destinations.

Cross Industry Migration – Cross industry migration happens when one industry gains at the cost of another. For example, advent of digital cameras resulted in massive decline of film rolls industry and saw big companies like Kodak having to shut down.

Migration Across Value Chain – Some phenomenon can result in industries at the down end of value chain gain at the cost of those at the upper end or vice versa. For example, high competition intensity in the Indian telecommunication space resulted in significant fall in price of mobile services, which in turn led to significant decline in shareholder value for telecom companies. However, this resulted in increased consumption of digital products and thus more traction for digital content providers.

Migration Across Companies in the Same Industry – Certain disruption may create new competitive advantage for one company or may remove a competitive advantage enjoyed by an existing player. This may result is value migrating from one company to another. For example, before advent of 2G technology, Research in Motion (Blackberry) enjoyed significant competitive advantage among corporate mobile users. Its mobile devices were the most efficient in accessing emails and other internet services. However, with the advent of 2G Technology many new smartphone manufacturers emerged. They were able to provide similar service. This eventually led to decline in shareholder value for Blackberry while its competitors such as Apple saw the value increasing.

Understanding value migration can help analysts identify suitable investment opportunities ahead of time and to exit from the loosing businesses.

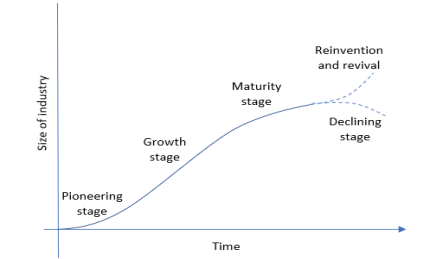

5.2 Business Life Cycle

Business life cycle refers to the various stages through which a business transitions through its journey from its emergence till its eventual decline.

Every industry typically goes through the following phases:

(a) Pioneering Stage – The industry is just taking shape. It is not widely adopted. The concept is still being proven or just been proven.

(b) Growth Stage – The concept is found viable and many customers start adopting the new product. As more and more customers adopt the product, the industry witness steep growth.

(c) Matured Stage – The industry has existed for long and most customers who can use the product are already using it. Number of new (potential) customers are relatively less.

(d) Declining Stage – Change in customer preference or a new technology replaces the industry’s product with a new product. At this juncture, the industry starts losing out to the alternatives.

(e) Reinvention and Revival – Although it is very rare, it is possible that the goods or services produced by the industry finds a new use in a different application and starts a new cycle all over again.

In the Indian context, call taxis can be looked at one example of an industry that has gone through all the phases over a period.

Call taxis in India started taking shape during the end of 20th century and early parts of 21st century. Aided by increased penetration of telephones and growing consumer income, call taxi services witnessed tremendous growth over the next decade. However, with the advent of app-based taxi aggregators, the industry declined significantly in size.

Every industry goes through the cycle and in turn causes significant displacement in the economy. The labor force working in one industry will have to reskill themselves and move to a new industry or find themselves out of workforce. Similarly, capacity will need to be redirected to a different use.

Although secular trends can be traced to business lifecycles, there are other disruptors that can affect the secular trend. For example, horizontal drilling technology enabled exploration of shale gas which brought a long-term decline in crude oil prices without causing any displacement of the goods being consumed.

Analysing and understanding secular trends help the analyst understand the long-term trajectory of the business.

However, in order to understand the medium term and short-term trends, analyst will have to focus on cyclical trends.

6. Understanding the Industry Landscape

Industry landscaping involves studying all the players in the industry and their interaction with each other. This includes understanding competitors, customers, suppliers, regulators, and emerging technologies. It also involves studying the differentiating factors between various competitors and customer’s preference.

Such a study will help the analyst understand how the industry may react to external market events. For example, in industries with low competition intensity, companies are likely to be able to transfer any increase in input cost to their customers. Thus, their profit margin is likely to remain intact. On the other hand, if the competition intensity is high, it may create pricing pressure which will likely reduce the profits.

Industry landscaping needs to be very comprehensive. While analysts can use their own frameworks, there are certain established frameworks that can help understand the industry landscape. These include the following:

(i) Michael Porter’s Five Force Model

(ii) PESTLE Analysis

(iii) BCG Matrix

(iv) SCP Analysis

The post Fundamentals of Industry Analysis – Cyclicality | Trends appeared first on Taxmann Blog.

source