Supply under GST refers to the taxable event that triggers the levy of Goods and Services Tax on transactions involving goods or services or both. As per Section 7 of the CGST Act, 2017, it includes all forms of supply such as sale, transfer, barter, exchange, licence, rental, lease, or disposal made or agreed to be made for a consideration in the course or furtherance of business. The concept of supply forms the foundation of the GST framework, replacing multiple taxable events under the earlier indirect tax regime—such as manufacture, sale of goods, and provision of services—with a single unified taxable event. Consequently, GST becomes applicable whenever there is a supply of goods or services or both, unless the transaction is specifically excluded or exempt under the law.

Table of Contents

- Introduction

- Supply – The Taxable Event in GST

- Forms of Supply

- Types of Supplies

- Types of Supplies in Case of Combination Supplies

Check out Taxmann's GST & Customs Law (Incorporating GST 2.0) which is a comprehensive, statute-based textbook that presents GST and Customs Law as a unified indirect tax and compliance framework. Fully updated with amendments up to 31st December 2025, the 13th Edition integrates the GST 2.0 reforms (September 2025), capturing the shift towards structural correction, rate rationalisation, and simplified, trust-based compliance. The book follows a concept-first, illustration-driven pedagogy, explaining each topic through statutory provisions, rule mechanics, numerical illustrations, and exam-oriented practice. Designed for commerce students, CA aspirants, faculty, and tax professionals, it serves as both a strong foundational text and a practical reference for execution.

1. Introduction

Under earlier indirect tax laws, there were two separate activities, i.e. manufacture or sale of goods and the provision of services. In the GST regime, the entire value of these two is taxed in an integrated manner by laying down one comprehensive taxable event i.e. “supply” – supply of goods or services or both. It means, the term “supply” refers to a broad term which merges all taxable activities of the earlier laws into a single activity. For Example – If Mr A has sold goods to B, then it is supply of goods. In this case, if A has manufactured the goods and then has sold to B, even then it is supply of goods. Similarly, if Mr Mohan took services of engineer for construction of his house, then it is also supply of services to Mr Mohan. Under GST, the scenario has been shifted from sales, service, manufacturing, etc. to one activity i.e. supply. Therefore, it can be said that now, there are two modes of supply which may attract GST and these are goods and services.

2. Supply – The Taxable Event in GST

Taxable event in a law is an event, the occurrence or happening of which triggers the imposition of tax. It means the incidence of tax arises only after the occurrence of the taxable event.

Before GST – Under the earlier indirect tax laws, Central excise was levied on “manufacture of goods”, VAT/CST was levied on “Sale of Goods”, Service tax was charged on “Services provided or agreed to be provided”, etc.

Under GST – According to Article 366(12A) of the Constitution of India, Goods and Services Tax (GST) is “Any tax on Supply of goods or services or both except taxes on Supply of the Alcoholic liquor for human consumption.” Therefore, under GST, the taxable event is “Supply of Goods or provision of Services or both”. As already stated, under GST the scenario has been shifted from multiple taxable event namely manufacture, sales, provision of services, etc. to one sole taxable activity i.e. Supply. The GST is applicable if there is Supply of goods or provision of Services or both.

3. Forms of Supply

Under GST, supply includes all forms of supply of goods or services or both. The concept of supply is the key stone of the GST architecture because the supply of anything other than goods or services does not attract GST. There are two forms of supply under GST namely, goods and services.

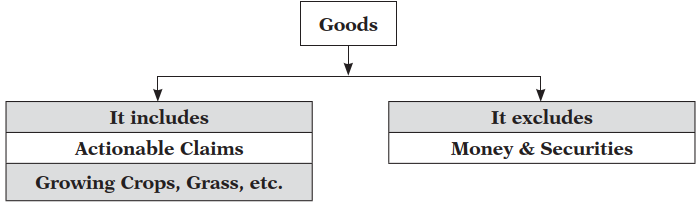

3.1 Goods

As per section 2(52) of CGST Act, 2017, “Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply.

Actionable Claim – The section 2(1) of CGST Act provides that the definition of actionable claims shall have the same meaning as assigned to it in section 3 of the Transfer of Property Act, 1882. As per section 3 of the Transfer of Property Act, 1882,

“actionable claim means a claim to any debt, other than a debt secured by mortgage of immovable property or by hypothecation or pledge of movable property, or to any beneficial interest in movable property not in the possession, either actual or constructive, of the claimant, which the civil courts recognise as affording grounds for relief, whether such debt or beneficial interest be existent, accruing, conditional or contingent.”

It may be noted that there are certain activities listed in Schedule III which are treated neither as Supply of goods nor as Supply of services. Actionable claims (other than lottery, betting & gambling) have been included in this Schedule. Thus, only lottery, betting & gambling shall be treated as Supply under GST. All the other actionable claims shall not be Supplies.

Money – As per section 2(75) of CGST Act,

“Money means the Indian legal tender or any foreign currency, cheque, promissory note, bill of exchange, letter of credit, draft, pay order, traveller cheque, money order, postal or electronic remittance or any other instrument recognised by the Reserve Bank of India when used as a consideration to settle an obligation or exchange with Indian legal tender of another denomination but shall not include any currency that is held for its numismatic value.”

Transaction in Money – The transaction in money is outside the ambit of GST as it is not included in the definition of goods/services. When we deposit principal amount in the bank or if such amount is withdrawn, then it is simply a transaction in money. These transactions do not constitute service & thus are not chargeable to GST. However, if a separate consideration is charged for these activities, then this consideration is subject to GST. For example – if Rs. 2000 note is exchanged for 20 notes of Rs. 100 then it is transaction in money. But, if in consideration Rs. 1950 is given, then GST becomes payable on Rs. 50.

Securities – The term “securities” shall have the same meaning as assigned to it in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956. As per this Act, the term securities include the following in India:

- Shares, scrips, stocks, bonds, debentures, debenture stock or other marketable securities of a like nature in or of any incorporated company or other body corporate

- Derivatives which includes

- Government security – a security created and issued by the Central Government or a State Government

- Units or any other instrument issued by any collective investment scheme to the investors in such schemes

- Units or any other such instrument issued to the investors under any mutual fund scheme but does not include any unit linked insurance policy which is a hybrid instrument providing for life risk cover and investments

- Security receipts issued under SARFAESI Act (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002)

- Securitised debt instruments (collateralised debt obligations, etc.)

- Such other instruments as may be declared by the Central Government to be securities; and

- Rights or interest in securities.

| Please note that Securities are neither goods nor Services. |

3.2 Service

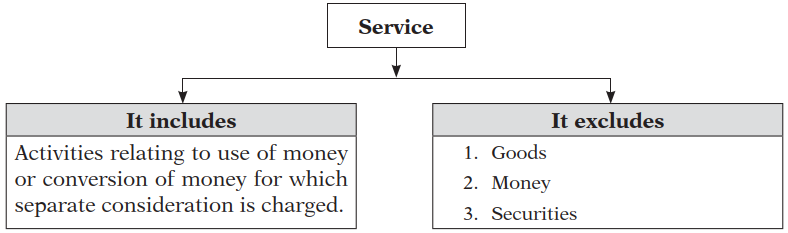

The term ‘Service’ has been defined under section 2(102) of CGST Act, 2017. As per this section,

“service means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged.”

It means the Service refers to anything other than goods, money and securities but includes activities relating to use of money or conversion of money for which separate consideration is charged.

Explanation to section 2(102)#

Statutory Provision – “For removal of doubts, it is hereby clarified that the expression ‘Services’ includes facilitating or arranging transactions in securities.”

Explanation – AS per the definition of goods and services, the securities are excluded from the definition of both ‘goods’ and ‘services’ in the CGST Act and they are neither goods nor services. However, facilitating or arranging transactions in securities is liable to GST. In order to clarify the same, the above explanation has been inserted to section 2(102).

Example – In relation to transactions in securities, if some service charges or service fees or documentation fees or broking charges or such like fees or charges are charged, then the same would be a consideration for provision of service and shall be chargeable to GST.

Note – Under GST, the supply should be of goods or services. Supply of anything other than goods or services does not attract GST.

| Supply to Be Classified Either as Goods or as Services |

| As stated above, supply should involve goods and/or Services viz. either as wholly goods or wholly services. Now, a question arises, what will happen where a supply involves both goods and services? The GST law provides that such supplies would be classifiable either as, wholly goods or wholly services. This classification has been provided in Schedule II of the Act, which has been discussed later in this article. |

4. Types of Supplies

As already stated in previous Para, the term supply under GST includes supply of goods as well as supply of services. This supply may be classified on various basis.

(a) On the basis of movement/flow

(a) Inward supply

(b) Outward supply

(b) On the basis of Continuity

(a) One time supply

(b) Continuous supply

(c) On the basis of taxability

(a) Taxable supply

(b) Non-taxable supply

(c) Exempt supply

(d) Zero-rated supply

(d) On the basis of Geographical location

(a) Intra-state supply

(b) Inter-state supply

(c) Supplies in territorial waters

(e) On the basis of Goods supplied in conjunction

(a) Composite supply

(b) Mixed supply

4.1 Types of Supplies on the Basis of Movement/Flow

Every transaction necessarily involves two parties namely supplier and recipient. When we consider a supply of goods/services from the point of view of either of the party, it may be classified as inward supply or outward supply.

(a) Inward Supply – In relation to a person, “inward supply” means receipt of goods or services or both, whether by purchase, acquisition or any other means with or without consideration.

(b) Outward Supply – In relation to a taxable person, “outward supply” means supply of goods or services or both, whether by sale, transfer, barter, exchange, licence, rental, lease or disposal or any other mode, made or agreed to be made by such person in the course or furtherance of business.

Example – Ravish Computers Ltd., a registered dealer has sold desktop computer to ABC Ltd. at a price of Rs. 26,000 plus GST. This single transaction of supply of computer constitutes “inward Supply” for recipient (i.e. for ABC Ltd.) and “Outward Supply” for the Supplier (i.e. for Ravish computers Ltd.)

4.2 Types of Supplies on the Basis of Continuity

The recurrence of a Supply is the basis for this classification:

(a) One-time Supply – It simply refers to Supply of goods or Services which is provided or agreed to be provided on non-recurrent basis as a Standalone Supply. For Example – when Mahesh purchases a machine from M/s. ABC, then it is one-time Supply. This category is required just to recognise the other type of Supply, which is continuous Supply.

(b) Continuous Supply – The continuous supply may be as regards goods as well as for services.

Continuous Supply of Goods – As per section 2(32) of CGST Act, 2017, “continuous supply of goods” means a supply of goods which is provided, or agreed to be provided, continuously or on recurrent basis, under a contract, whether or not by means of a wire, cable, pipeline or other conduit, and for which the supplier invoices the recipient on a regular or periodic basis.

Continuous Supply of Services – As per section 2(33) of CGST Act, 2017, “continuous supply of services” means a supply of services which is provided, or agreed to be provided, continuously or on recurrent basis, under a contract, for a period exceeding three months with periodic payment obligations.

Example – Kanika uses LPG stove and is a registered customer with Shivani Enterprises, a dealer of LPG Cylinders. She acquires two cylinders every month on regular basis. It is the example of one-time supply where every supply of cylinder is a separate transaction. On the other hand, Ms Tania has taken PNG connection at her kitchen from Indraprastha Gas Limited. The billing is done monthly on the basis of meter reading. It is the case of continuous supply of goods.

4.3 Types of Supplies on the Basis of Taxability

The scope of supply has been given in section 7 of CGST Act, 2017. Even if an activity is a supply, it is not necessary that the same is subject to GST. On this basis, there can be following types of supplies:

(a) Taxable Supply – As per section 2(108) of CGST Act,

“Taxable Supply refers to a Supply of Goods and/or Services which is leviable to tax under CGST Act”.

(b) Non-Taxable Supply – As per section 2(78) of CGST Act,

“Non-Taxable Supply means a Supply of Goods or Services or both which is not leviable to tax under CGST Act or under the IGST Act”.

(c) Exempt Supply – As per section 2(47) of CGST Act,

“Exempt Supply means a Supply of any Goods or Services or both which attracts Nil rate of tax or which may be wholly exempt from tax under Section 11, or under section 6 of IGST Act, and includes non-taxable Supply”.

(d) Zero Rated Supply – It is Supply of any Goods and/or Services on which no tax is payable but input tax credit pertaining to that Supply is admissible. As per Section 16(1) of IGST Act, 2017, “zero rated supply” means any of the following supplies of goods or services or both, namely:

(a) export of goods or services or both; or

(b) supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

4.4 On the basis of Geographical location

When we consider the movement of Supply geographically, it can be of three types namely Inter-State Supply, Intra-State Supply and Supplies in the territorial waters.

(1) Inter-State Supply – As per Section 7(1) of IGST Act, Subject to the provisions of section 10, supply of goods, where the location of the supplier and the place of supply are in:

(a) two different States;

(b) two different Union territories; or

(c) a State and a Union territory,

shall be treated as a supply of goods in the course of inter-State trade or commerce.

Similarly, as per Section 7(3), Subject to the provisions of section 12, supply of services, where the location of the supplier and the place of supply are in:

(a) two different States;

(b) two different Union territories; or

(c) a State and a Union territory,

shall be treated as a supply of services in the course of inter-State trade or commerce.

(2) Intra-State Supply – As per Section 8(1) of IGST Act, Subject to the provisions of section 10, supply of goods where the location of the supplier and the place of supply of goods are in the same State or same Union territory shall be treated as intra-State supply:

Provided that the following supply of goods shall not be treated as intra-State supply, namely:

(i) supply of goods to or by a Special Economic Zone developer or a Special Economic Zone unit;

(ii) goods imported into the territory of India till they cross the customs frontiers of India; or

(iii) supplies made to a tourist referred to in section 15.

(3) Supplies in the Territorial Waters – As per Section 9 of IGST Act, Notwithstanding anything contained in this Act:

(a) where the location of the supplier is in the territorial waters, the location of such supplier; or

(b) where the place of supply is in the territorial waters, the place of supply, shall, for the purposes of this Act, be deemed to be in the coastal State or Union territory where the nearest point of the appropriate baseline is located.

5. Types of Supplies in Case of Combination Supplies

The GST is payable on individual goods or Services or both at the notified rates. For example – The Tooth-paste and Tooth-brush are liable to GST @ 12% and 18% respectively. It means the GST on these items will be calculated accordingly. Sometimes, two or more goods or Services are supplied in combination at a Consolidated price. In this case, a question arises about the rate of GST to be levied as the goods/services in package may be subjected to different rates of tax. For example:

(a) A desktop computer (GST @ 28%) and a wooden table (GST @ 18%) are offered by supplier at a consolidated price of Rs. 52,500.

(b) Supply of LCD with warranty and maintenance for 1 year again at a consolidated price.

For the purpose of taxability, the CGST Act, classifies these “Combination Supplies” into two types:

- Composite Supply

- Mixed Supply

5.1 Composite Supply

As per section 2(30) of CGST Act, 2017,

“Composite Supply” means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply.

The following are the basic features of a composite supply:

(a) It should be the supply made by taxable person to a recipient.

(b) It should consist of two or more taxable supplies of Goods or services or both.

(c) The combination should be naturally bundled and supplied in conjunction with each other in the ordinary course of business.

- The Supplied in conjunction means that they should be occurring in the same point in time and space.

|

(d) Out of two naturally bundled supplies, one should be a principal supply.

- Where goods are packed and transported with insurance, the supply of goods, packing materials, transport and insurance is a composite supply and supply of goods is a principal supply.

- Principal Supply means supply which forms the predominant element of the composite supply and other parts of the supply are only ancillary or supportive to that predominant part.

|

Examples on Composite Supply

| Example 1 |

| Supply – Prakash buys LCD and also gets warranty and a maintenance contract with the LCD.

Comment – This supply is a composite supply. The supply of LCD is the principal supply and warranty/maintenance services are ancillary. |

| Example 2 |

| Supply – Samrat Hotel in Shimla, provides 4 days-3 nights package at Rs. 8,000 wherein the facility of breakfast and dinner is provided along with the room accommodation.

Comment – It is composite supply since the supply of breakfast and dinner with the accommodation in the hotel are naturally bundled. |

| Example 3 |

| Supply – The Xiaomi Communication Co. Ltd. has recently launched a mobile phone with the brand name “Redmi Note 4”. The company supplies the accessories, earphone and charger along with the handset.

Comment – The supply of earphone and charger with the mobile phone handset are naturally bundled. This supply qualifies as “composite Supply.” The Supply of mobile phone is the principal supply. |

Clarification by CBIC

CBIC has clarified as to what constitutes the principal supply in the given composite supplies:

| 1. |

Activity/Transaction: |

| Supply of printed books, pamphlets, brochures, envelopes, annual reports, leaflets, cartons, boxes etc., printed with design, logo, name, address or other contents supplied by the recipient of such printed goods. |

|

Principal Supply: |

| Supply of Service – In the case of printing of books, pamphlets, brochures, annual reports, and the like, where only content is supplied by the publisher or the person who owns the usage rights to the intangible inputs while the physical inputs including paper used for printing belong to the printer, supply of printing [of the content supplied by the recipient of supply] is the principal supply and therefore such supplies would constitute supply of service.

Supply of Goods – In case of supply of printed envelopes, letter cards, printed boxes, tissues, napkins, wallpaper etc. by the printer using its physical inputs including paper to print the design, logo etc. supplied by the recipient of goods, predominant supply is supply of goods and the supply of printing of the content [supplied by the recipient of supply] is ancillary to the principal supply of goods and therefore such supplies would constitute supply of goods.

[Circular No. 11/11/2017-GST dated 20-10-2017] |

| 2. |

Activity/Transaction: |

| Activity of Bus Body Building |

| Principal Supply: |

| The principal supply may be determined on the basis of facts and circumstances of each case [Circular No. 34/8/2018-GST dated 01-03-2018] |

| 3. |

Activity/Transaction: |

| Retreading of Tyres |

| Principal Supply: |

| Supply of Service – Pre-dominant element is process of retreading which is a supply of service. Rubber used for retreading is an ancillary supply.

Supply of Goods – Supply of retreaded tyres, where the old tyres belong to the supplier of retreaded tyres, is a supply of goods.

[Circular No. 34/8/2018-GST dated 01-03-2018] |

5.2 Mixed Supply

As per Section 2(74),

“Mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply.”

The essence of the definition is that there should be supply of two or more individual goods or services or any combination thereof, in conjunction with each other. In fact, in case of mixed supplies, the goods/services which are supplied to the recipient at one price can be supplied individually. In other words, the individual supplies are independent of each other and are not naturally bundled.

In nutshell, a supply of more than one goods and/or services as a bundle will be reckoned as mixed supply if the following conditions are fulfilled:

(i) Such goods/or services are supplied for a single price.

(ii) They are not naturally bundled together and

(iii) It does not qualify as composite supply.

Examples on Mixed Supply:

| Example 4 |

| Supply – A gift pack comprising of canned foods, sweets, chocolates, cakes, dry fruits, aerated drinks and fruit juices supplied for a single price.

Comment – It is an example of mixed supply as all these goods can be sold independently. |

| Example 5 |

| Supply – Rent deed executed for renting of the different floors of a building, one for residence and another for commercial purpose to the same person.

Comment – It will be treated as mixed supply as the two floors could have been rented independently. |

| Example 6 |

| Supply – A supply of a package Comprising of shirt, trouser, tie and belt for a single price.

Comment – It is a mixed supply. The reason being each of these items can be supplied separately and is not dependent on any other. |

| Works Contract and Restaurant Services |

| 1. As per section 2(119) of CGST Act, 2017, “Works contract means a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract.”

2. Works contract and restaurant services are the classic example of composite supplies. However, the GST law identifies both as supply of services [as per Schedule II] |

# Inserted by the CGST (Amendment) Act, 2018, dated 30-8-2018, w.e.f. 1-2-2019 vide Notification No. 02/2019-Central Tax, dated 29-1-2019.

The post Supply Under GST – Meaning | Types | Taxable Event appeared first on Taxmann Blog.

source